Private Activity Bonds and AMT: What Investors Need to Know

Key Takeaways

- PAB interest is tax-exempt under regular tax but taxable under AMT

- Large PAB holdings can trigger significant AMT liability

- General obligation municipal bonds do not trigger AMT — PABs are the exception

- The AMT adjustment equals the full amount of PAB interest received

- Model the AMT impact before making large PAB investments

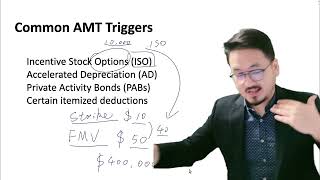

Private Activity Bonds and AMT

Private Activity Bonds (PABs) are municipal bonds issued to finance projects with private benefit — such as local airport expansions, affordable housing developments, or sports facilities. Interest from most municipal bonds is tax-exempt under the regular federal tax system. However, PAB interest is added back when calculating Alternative Minimum Taxable Income (AMTI).

How PABs Trigger AMT

Under the regular tax system, if you invest $1 million in PABs earning 5% interest ($50,000/year), that interest is tax-exempt and does not appear on your Form 1040 as taxable income. Under the AMT system, that same $50,000 is added back to your income for AMT calculation purposes.

This can create a significant AMT liability for investors with large PAB holdings. The higher your PAB interest income, the larger the AMT adjustment, potentially triggering AMT that exceeds your regular tax.

Planning Considerations

If you hold substantial PAB investments, monitor your AMT exposure annually. Consider diversifying into general obligation municipal bonds (which are exempt from both regular tax and AMT) rather than concentrating in PABs. Consult a tax advisor to model the AMT impact before making large PAB investments.

File Your LLC Taxes Now

Generate your IRS Form 5472 + pro forma Form 1120 in 15 minutes. Every field linked to official IRS instructions. $49, no CPA needed.