Married Filing Jointly with Non-Resident Alien Spouse: MFJ Qualification Rules

Key Takeaways

- Legal marriage on December 31 determines your filing status for the entire year

- Living apart does NOT equal legal separation — only a court decree changes your status

- U.S. citizens can elect MFJ with NRA spouses by treating them as U.S. residents

- The NRA election subjects the foreign spouse's worldwide income to U.S. tax

- Carefully weigh the benefits (higher deductions, more credits) against increased tax exposure

Marriage Definition for Tax Purposes

For IRS purposes, you are considered married if on the last day of the tax year you are legally married and either living together (cohabiting), living apart but not legally separated by a divorce decree, or legally separated under a decree that is not yet final. Simply living apart does not make you unmarried — only a final divorce decree or legal separation changes your marital status.

MFJ with a Non-Resident Alien Spouse

If you are a U.S. citizen or resident married to a non-resident alien (NRA), you can elect to file jointly by treating the NRA spouse as a U.S. resident for the entire tax year. This election is made on your joint return and subjects both spouses to U.S. taxation on their worldwide income.

While this can provide tax benefits (higher standard deduction, access to more credits), it also means the NRA spouse's foreign income is now subject to U.S. tax. This election should be made carefully, considering both the benefits and the additional tax exposure.

File Your LLC Taxes Now

Generate your IRS Form 5472 + pro forma Form 1120 in 15 minutes. Every field linked to official IRS instructions. $49, no CPA needed.

More on Filing Status Guide

5:21

5:21Form 1040 Filing Status: Qualifying Surviving Spouse Explained

6:05

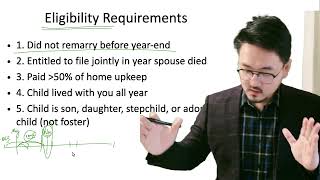

6:05Qualifying Surviving Spouse Eligibility: Did Not Remarry Requirement (Part 1)

5:33

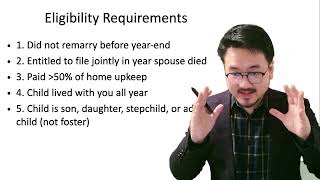

5:33Qualifying Surviving Spouse: Entitled to File Requirement (Part 2)

12:42

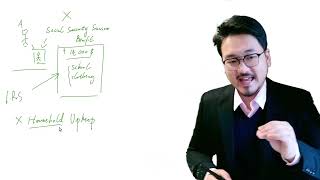

12:42Qualifying Surviving Spouse: Paid More Than 50% Cost of Home (Part 3)

3:58

3:58Qualifying Surviving Spouse: Cost of Home Calculation Example (Part 4)

6:13

6:13