Qualifying Surviving Spouse Eligibility: Did Not Remarry Requirement (Part 1)

Key Takeaways

- Must not remarry before the end of the tax year to claim QSS

- QSS is available for two years following the year of spouse's death

- Remarrying ends QSS eligibility but opens MFJ with new spouse

- Must continue to meet all other QSS requirements each year

- This is a financial decision — weigh the tax implications carefully

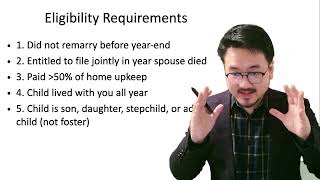

QSS Requirement: Did Not Remarry

The first eligibility requirement for Qualifying Surviving Spouse status is that you must not have remarried before the end of the tax year. If you remained single throughout the year while raising your dependent child, you can claim QSS for that year.

For example, if your spouse passed away in May 2023 and you stayed single through all of 2024, you can file as QSS for 2024. However, if you remarried in November 2024, you lose QSS eligibility for that year and would instead file jointly with your new spouse or choose another applicable status.

Financial Decision Making

The decision to remarry has tax implications beyond the personal. Remarrying ends QSS eligibility but opens up MFJ filing with the new spouse. In many cases, this is still beneficial — but the two-year QSS window is specifically designed to ease the financial transition after a spouse's death, and the tax rates mirror the favorable MFJ brackets.

File Your LLC Taxes Now

Generate your IRS Form 5472 + pro forma Form 1120 in 15 minutes. Every field linked to official IRS instructions. $49, no CPA needed.

More on Filing Status Guide

5:21

5:21Form 1040 Filing Status: Qualifying Surviving Spouse Explained

5:33

5:33Qualifying Surviving Spouse: Entitled to File Requirement (Part 2)

12:42

12:42Qualifying Surviving Spouse: Paid More Than 50% Cost of Home (Part 3)

3:58

3:58Qualifying Surviving Spouse: Cost of Home Calculation Example (Part 4)

6:13

6:13Qualifying Surviving Spouse: Child's Survivor Benefits Rules (Part 5)

13:17

13:17