How the General Business Credit Works: Form 3800 Mechanics

Key Takeaways

- Calculate each credit separately, then combine on Form 3800

- GBC limitation = net tax minus greater of TMT or 25% of net tax above $25,000

- Allowable credit is the lesser of total credits or the limitation

- Excess carries back 1 year or forward 20 years

- Oldest credits are applied first (FIFO order)

GBC Calculation Process

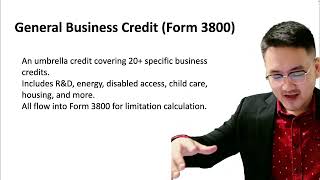

To calculate your General Business Credit, start by computing each individual credit on its respective form (e.g., Form 6765 for R&D, Form 3468 for energy). Bring each credit amount to Form 3800 and add them together to get your total current-year GBC.

Next, determine your GBC limitation: net income tax minus the greater of your tentative minimum tax or 25% of net regular tax above $25,000. The allowable GBC for the year is the lesser of your total credits or the limitation amount.

Carryback and Carryforward

If your total credits exceed the limitation, the excess is not wasted. You can carry the excess back 1 year (amending the prior year's return) or carry it forward up to 20 years. This flexibility ensures that business credits provide long-term value even in years when your tax liability is insufficient to absorb them all.

Credits are applied in chronological order — oldest carryforwards are used first, then current-year credits, then carrybacks.

File Your LLC Taxes Now

Generate your IRS Form 5472 + pro forma Form 1120 in 15 minutes. Every field linked to official IRS instructions. $49, no CPA needed.

More on Tax Credits (FTC, GBC)

3:42

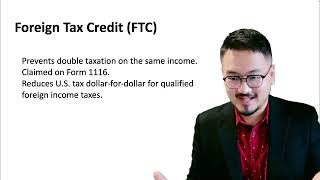

3:42Foreign Tax Credit: Introduction to Avoiding Double Taxation

4:28

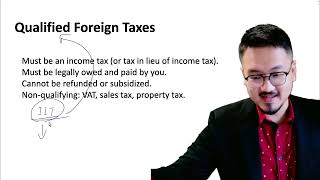

4:28Which Foreign Taxes Qualify for the Tax Credit?

5:15

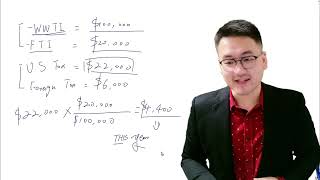

5:15FTC Allowed Formula: How to Calculate Your Foreign Tax Credit

3:55

3:55General Business Credit Introduction and Overview

4:42

4:42Form 3800: Filing the General Business Credit

6:08

6:08