Key Takeaways

- Simple example: $25K R&D credit against $40K tax liability = full $25K used

- If credits exceed the limitation, excess carries forward up to 20 years

- No AMT and no other credits simplifies the calculation significantly

- Real-world calculations involve multiple credits and AMT interactions

- Professional assistance recommended for complex GBC situations

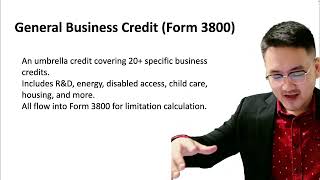

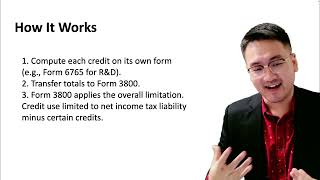

Simplified GBC Calculation Example

Suppose your startup has a $25,000 R&D credit (calculated on Form 6765). Your net income tax liability is $40,000, with no other credits and no AMT. The GBC limitation is $40,000 minus zero (no TMT, no other credits) = $40,000.

Since your $25,000 credit is less than the $40,000 limitation, you can use the full $25,000 credit, reducing your tax from $40,000 to $15,000. If your R&D credit had been $50,000 instead, you could only use $40,000 this year, with the remaining $10,000 carrying forward.

Real-World Complexity

In practice, calculations are more complex due to multiple credits, AMT considerations, and interactions between current-year credits and carryovers. However, the fundamental logic remains the same: calculate each credit, combine them, apply the limitation, and carry forward any excess.

A tax professional is strongly recommended for GBC calculations, especially when multiple credits, AMT, and carryovers from prior years are involved.

File Your LLC Taxes Now

Generate your IRS Form 5472 + pro forma Form 1120 in 15 minutes. Every field linked to official IRS instructions. $49, no CPA needed.

More on Tax Credits (FTC, GBC)

3:42

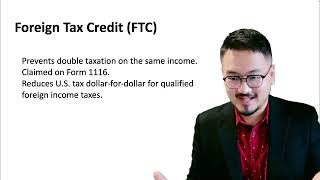

3:42Foreign Tax Credit: Introduction to Avoiding Double Taxation

4:28

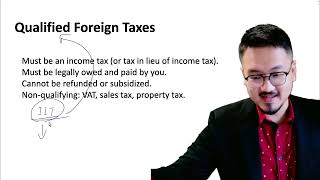

4:28Which Foreign Taxes Qualify for the Tax Credit?

5:15

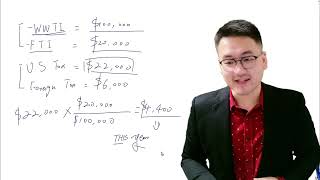

5:15FTC Allowed Formula: How to Calculate Your Foreign Tax Credit

3:55

3:55General Business Credit Introduction and Overview

4:42

4:42Form 3800: Filing the General Business Credit

5:33

5:33